Introduction

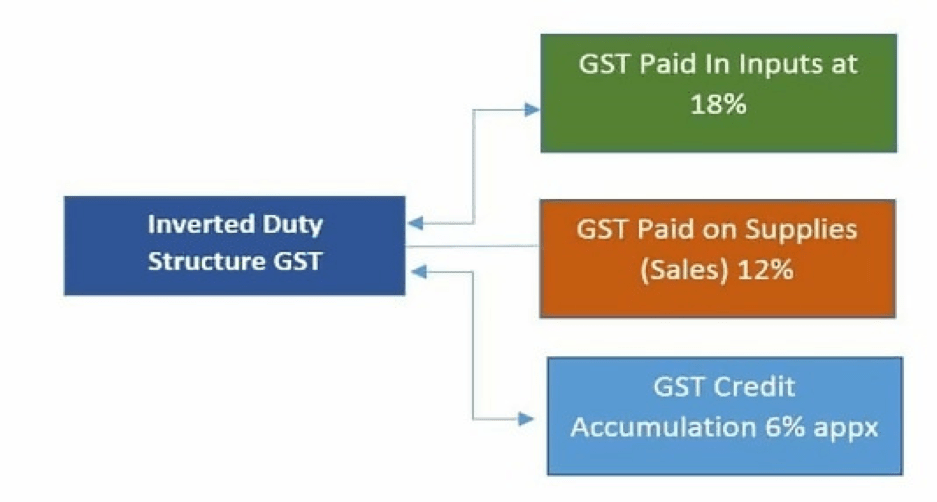

The GST Act does not define anything like Inverted duty structure. The term ‘Inverted Tax Structure’ refers to a situation where the rate of tax on inputs purchased (i.e. GST Rate paid on inputs received) is more than the rate of tax (i.e. GST Rate Payable on outward supplies) on outward supplies.

Example:

Krishna Ltd is a company which is manufacturing Inverter, for which the company buys input raw material at 18 % say GST paid is Rs. 1,00,000. The final product is inverter on which say GST Rate is 12 % and GST payable is Rs. 65,000. In this situation, Krishna Ltd. is paying more GST on inputs used then the manufactured output product inverter. This situation is called Inverted duty structure of GST.

GST Refund in case of inverted duty structure

As per Section 54(3) of the CGST Act, 2017, a registered person may claim a refund of the unutilized input tax credit on account of Inverted Duty Structure (Rate of tax on Inputs > Rate of tax on Outputs & Output services) at the end of any tax period. A tax period is a period for which return is required to be furnished. In following cases no refund of the unutilized input tax credit shall be allowed:

- If output supplies are nil rated or fully exempt supplies.

- If the goods are exported out of India are subject to export duty.

- If the supplier of goods or services or both avails of drawback in respect if the central tax or claims a refund of IGST on such supplies.

- Vide notification No. 15/2017- Central tax (rates), it has been notified that no refund of the unutilized input tax credit shall be allowed under sub-section (3) of section 54 of the said Central Goods and Services Tax Act, in case of a supply of Construction Services.

- Following supplies of goods or services as notified by council vide notification no. 5/2017-Central tax (Rate):

| Sr.No. | Tariff item, heading, subheading or Chapter | Description of Goods |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 8 | 8601 | Rail locomotives powered from an external source of electricity or by electric accumulators |

| 9 | 8602 | Other rail locomotives; locomotive tenders; such as Diesel-electric locomotives, Steam locomotives and tenders thereof |

| 10 | 8603 | Self-propelled railway or tramway coaches, vans and trucks, other than those of heading 8604 |

| 11 | 8604 | Railway or tramway maintenance or service vehicles, whether or not self-propelled (for example, workshops, cranes, ballast tampers,trackliners, testing coaches and track inspection vehicles) |

| 12 | 8605 | Railway or tramway passenger coaches, not self-propelled; luggage vans, post office coaches and other special purpose railway or tramway coaches, not self-propelled (excluding those of heading 8604) |

| 13 | 8606 | Railway or tramway goods vans and wagons, not self-propelled |

| 14 | 8607 | Parts of railway or tramway locomotives or rolling-stock; such as Bogies, bissel-bogies, axles and wheels, and parts thereof |

| 15 | 8608 | Railway or tramway track fixtures and fittings; mechanical (including electro-mechanical) signalling, safety or traffic control equipment for railways, tramways, roads, inland waterways, parking facilities, port installations or airfields; parts of the foregoing |

However, Vide Notification No. 20/2018-Central Tax (Rate), dated 26.7.2018, Government has allowed the refund claim from 1st August 2018 on accumulated ITC due to inverted duty structure due to supplies received of goods mentioned in Serial no. 1, 2, 3, 4, 5, 6 & 7. But accumulated unutilized ITC on inward supplies in respect of goods mentioned above till 31st July 2018 shall lapse. By doing this government has allowed the claim of refund on ITC accumulated due to inverted duty structure to the textile industry.

Inputs for which refund is allowed

Notification no. 26/2018 make changes in Rule 89(5) with retrospective effect from 1st July 2017 and allow refund only for the inputs of goods. Input doesn’t include input services and capital goods for this purpose.

As per circular no. 79/53/2018- GST, Net ITC includes ITC of all inputs whether or not used directly consumed in the manufacturing process. An input tax credit of the GST paid on inputs shall be available to a registered person as long as he/she uses or intends to use such inputs for the purposes of his/her business and there is no specific restriction on the availment of such ITC under section 17(5) of CGST Act. And thus ITC on stores and spares, packing materials, materials purchased for machinery repairs, printing and stationery items are thus included in Net ITC for calculation of refund.

Calculation of maximum refund available

Maximum Refund Amount = (Turnover of inverted rated supply of goods and services X Net input tax credit / Adjusted total turnover) – Tax payable on such inverted rated supply of goods and services

Where,

- “Net ITC” shall mean input tax credit availed on inputs during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both.

- “Turnover of inverted rated supply of goods” means the value of the inverted supply of goods made during the relevant period.

- “Tax payable on such inverted rated supply of goods” means the tax payable on such inverted rated supply of goods under the same head, i.e. IGST, CGST, SGST.

- “Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under clause (112) of section 2 of CGST Act, excluding the value of exempt supplies other than inverted-rated supplies, during the relevant period.

- “Relevant period” means the period for which the claim has been filed.

Let us understand the above formula with an example:

Details of Inward supplies:

| Particulars | Value | GST Rate | GST (ITC) |

| Inward supplies used for the manufacture of good which is taxed at 5% | 200Lakhs | 12% | 24 Lakhs |

| Inward supplies used for the manufacture of good which is taxed at 18% | 150 Lakhs | 18% | 27 Lakhs |

| Total ITC | 51 Lakh |

Details of output supplies:

| Particulars | Value | GST Rate | GST (Liability) |

| Turnover of inverted rated supply taxed at 5% | 300 Lakhs | 5% | 15 Lakhs |

| Turnover of other supply taxed at 18% | 200 Lakhs | 18% | 36 Lakhs |

| Total Turnover | 500 Lakhs | 51 Lakh |

In the above example Net ITC will Rs. 51 Lakhs mentioned in the first table. Inverted turnover will be Rs. 300 Lakhs and total adjusted turnover are Rs. 500 Lakhs. Tax payable on inverted duty supply will be Rs. 15 Lakhs. The maximum available refund amount shall be calculated as under:

Maximum available refund = (300 x 51/500) – 15 i.e. Rs. 15.60 Lakhs.

Procedure of claiming refund

GSTR-1 & GSTR-3B has to be filed for the tax period for which a tax payer wants to apply for Refund of accumulated ITC.

The refund application must be filed in prescribed form RFD-01A. RFD-01A is a temporary return form introduced in place of RFD-01.

Steps:

- File the RFD-01A form on GST portal. ARN will be generated by the GST portal.

- Take the print out of the duly filed application form and ARN generated from GST portal.

- Submit the printed documents with relevant supporting documentation to the jurisdictional authority.

- Tax officer will process the refund application. After a successful process of application refund will be disbursed manually.

- If jurisdiction authority of the state or central is not allotted yet, the tax payer should approach Nodal officer of the respective state/central.

Time period for refund application

Application for refund shall be filed on a monthly basis in form RFD-01A. If tax payers turnover is up to 1.5 crores and he has opted for a quarterly return, then he can file refund application on a quarterly basis. But, RFD-01A has to be filled within two years from the end of financial years in which such claim of refund arises.

As per circular no. 37/11/2018, refund application for export may be filed for one calendar month/quarter by clubbing successive calendar months/quarters. However, it cannot be clubbed between months/quarters of different financial years. The same provisions can be applied to inverted duty structure also.

FAQs

The term ‘Inverted Tax Structure‘ refers to a situation where the rate of tax on inputs purchased (i.e.GST Rate paid on inputs received) is more than the rate of tax (i.e. GST Rate Payable on outward supplies) on outward supplies.

Yes, refund is allowed in case of inverted duty structure subject to certain conditions. Registered person has to apply for refund as per the procedure provided.

Computation of GST ITC Refund of ITC Accumulated Due to Inverted Tax Structure| GST Refund. Maximum Refund Amount = {(Turnover of inverted rated supply of goods and services) x Net ITC ÷ Adjusted Total Turnover} – tax payable on such inverted rated supply of goods and services.

No, refund is allowed only for GST paid on input goods. Notification no. 26/2018 make changes in Rule 89(5) with retrospective effect from 1st July 2017 and allow refund only for the inputs of goods. Input doesn’t include input services and capital goods for this purpose.